The regional analysis displays a whole spectrum of Discounters’ market positions, from leader (Western and Eastern Europe) to supporting channel (LATAM) and niche player (Asia). So, we took a more detailed look into individual countries to gain more insight into patterns in the FMCG market.

Our data offer the unique opportunity to examine different hypotheses as to why Discounters are the winners in the FMCG market. In our analysis, we focused on the unique selling propositions attributed to Discounters, such as low price and high share of private labels in their assortment. In addition, the availability of data from different countries allowed us to raise and more importantly, answer several questions, for example on the market penetration of Discounters and how it affects the market shares of other participants.

Does a higher market penetration of Discounters also result in a stronger market share?

Can the market share of Discounters be linked to a lower price index?

Is the penetration of private labels generally a sign for a lower price index?

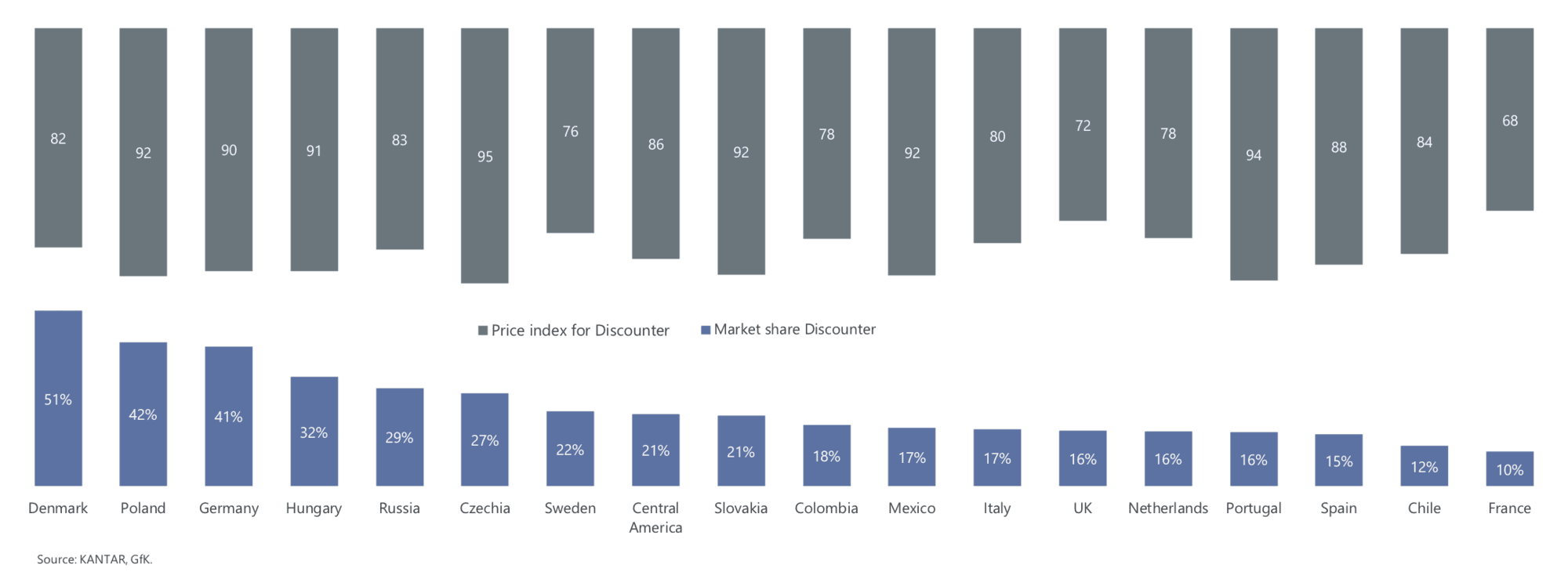

Market Penetration of Discounters in Denmark:

Our first analysis lead to a rather unsurprising result: The market share of Discounters and their market penetration are related. For example, where Discounters achieve a market share of more than 25%, they reach almost every household. Denmark is No. 1 with a market share for Discounters of 51% and a market penetration of 98%.

The data for Austria, Russia and Germany – just to name a few – show a similar pattern. But even in countries such as Spain or the United Kingdom, where Discounters have a rather low market share of 15% (Spain) and 16% (UK), Discounters achieve a significant market penetration of over 85%.

In France, where Hypermarkets dominate, Discounters account for only 10% of market share, but still reach a market penetration of 68%. These results show that market penetration is not the only success factor for Discounters. However, a majority of consumers to some degree are already shopping at Discounters, which can be seen as a good starting point to further increase market share and increase the revenue potential.

This is one unique selling proposition of Discounters and a clear differentiator from competitors such as Supermarkets or Hypermarkets. But does the different country data provide an indication if the price positioning* for Discounters relates to their market share? Are Discounters cheaper where their market position is low - and vice versa?

* price positioning /price index: Unit Price in Total food categories for Discounters versus price in total food categories in Hypermarkets and Supermarkets

The data for FMCG categories from different countries allows to draw some conclusions: For example, if the market share for Discounters is rather low, the price index of Discounters compared to Supermarkets and Hypermarkets is low, too.

The French market can, again, serve as an example: It is dominated by Hypermarkets with Discounters showing a significantly lower price index compared to Supermarkets and Hypermarkets. The data for the UK reveals a similar pattern: A market share of 16% for Discounters comes with a price index of 72.

Looking at the FMCG markets in Denmark, Poland and Germany, where Discounters have a significant market share above 40%, price indices for Discounters range from 82 (Denmark) to 90 (Germany) and 92 (Poland). To “globalize” the picture: A price index of 92 can also be seen in Mexico and Slovakia, with low market shares of 17% (Mexico) and 21% (Slovakia).

In summary – yes, discount means low price. This is valid for all countries we analyzed. However, the price index of Discounters versus the Discounters’ market share differs considerably. In countries with a lower market share, the pricing of Discounters is also much cheaper compared to Supermarkets and Hypermarkets. This could help Discounters to increase their market share. In countries with a higher market share for Discounters, price indices of Discounters versus Supermarkets and Hypermarkets tend to converge.

The data does not offer a final recipe for success or success pattern for the rise of Discounters. Either way is possible: Discounters might have used lower prices to increase their market share, or Supermarkets and Hypermarkets reacted to the market share of Discounters by introducing low-price private labels.

Given that the data on price and market position did not provide clear answers on the success factors of Discounters, we turn to a historically strong selling proposition of Discounters: private labels. But are private labels still valid success factors these days?

Over the past years, Supermarkets and Hypermarkets have been adding more private labels to their product range, while Discounters, in turn, often increased the share of brands in their assortment. Nonetheless, private labels remain the domain of Discounters.

This raises the question, whether a high share of private labels equals to a high market share for Discounters – and whether this is the success factor for the rise of Discounters.

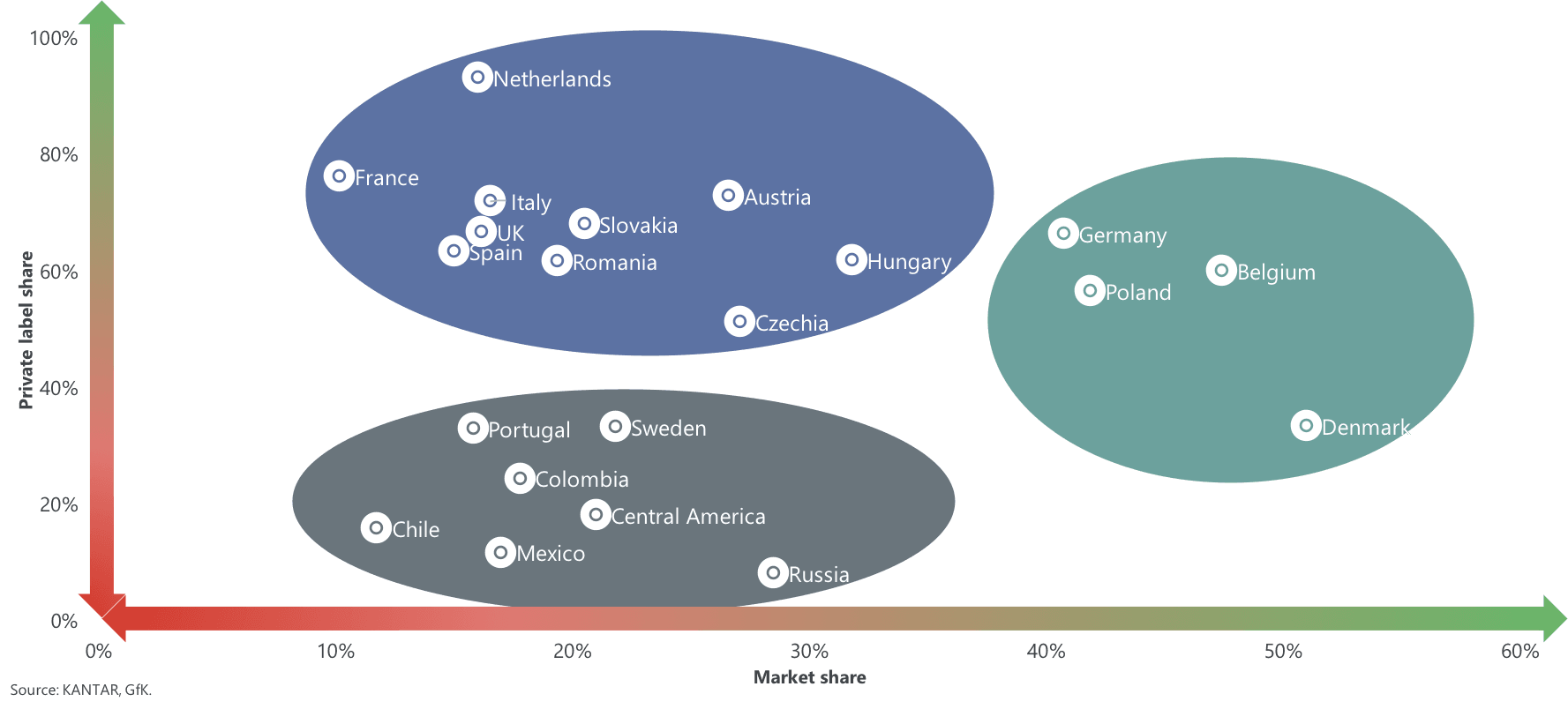

Once again, the data do not show any correlation. However, clustering countries along market and private label share provides additional insights: For example, we see countries like Germany, Poland, Belgium and Denmark with a very high market share for Discounters (up to 51% in Denmark) and mid to lower shares of private labels. Characteristic for these countries is the strength of a local Discounter (e.g. Biedronka in Poland, Colruyt in Belgium) and the overall strength of the well-known brands Lidl or Aldi (especially in their home market Germany).

In the Netherlands, the GfK Consumer Panel records a low market share for Discounters (16%) and a high share of private labels (93%). Italy, UK and Spain can also be counted into this cluster with low or mid-range market shares, but private label shares above 40%. This cluster sees brands like Aldi or Lidl active in the respective markets, but far from a leading or dominating position.

The third cluster is comprised of countries such as Russia, Portugal, Colombia and Mexico with a market share below 30% and a private label share below 40%. In Russia, data reveal the lowest market share for Discounters with only 28% and the lowest share for private labels with only 8%. The reason for this development, especially in Russia, might be the lack of a dominating multi-national Discounter.

For Discounters planning to enter a country or trying to expand their market share, private labels per se cannot serve as the key success factor. However, they do offer growth potential.

In addition, the potential growth through private labels is not necessarily linked to low price as our final country analysis of success patterns shows: Does low price result in a high share of private labels for Discounters?

Here, the data display a very mixed picture and all possible variations. For example, Czechia (Czech Republic) and Poland see a relatively high private label share and a relatively high price index for Discounters versus Supermarkets and Hypermarkets.

For countries like Italy, the UK and France, data show a relatively high private label share and a low price index. Countries in the LATAM region – Colombia, Mexico, and Chile – reveal a low private label share and different price indices for Discounters versus Supermarkets and Discounters.

Having analyzed the rise of Discounters in a global country comparison, let us once again focus on insights into the success of Discounters in Europe.