The growth rate of the global FMCG market closely follows the development of the global gross domestic product (GDP). As a result, we see the global FMCG growth rate for 2019 at +2.4%, down from +2.6% in 2018.

Who is fueling this (small) growth?

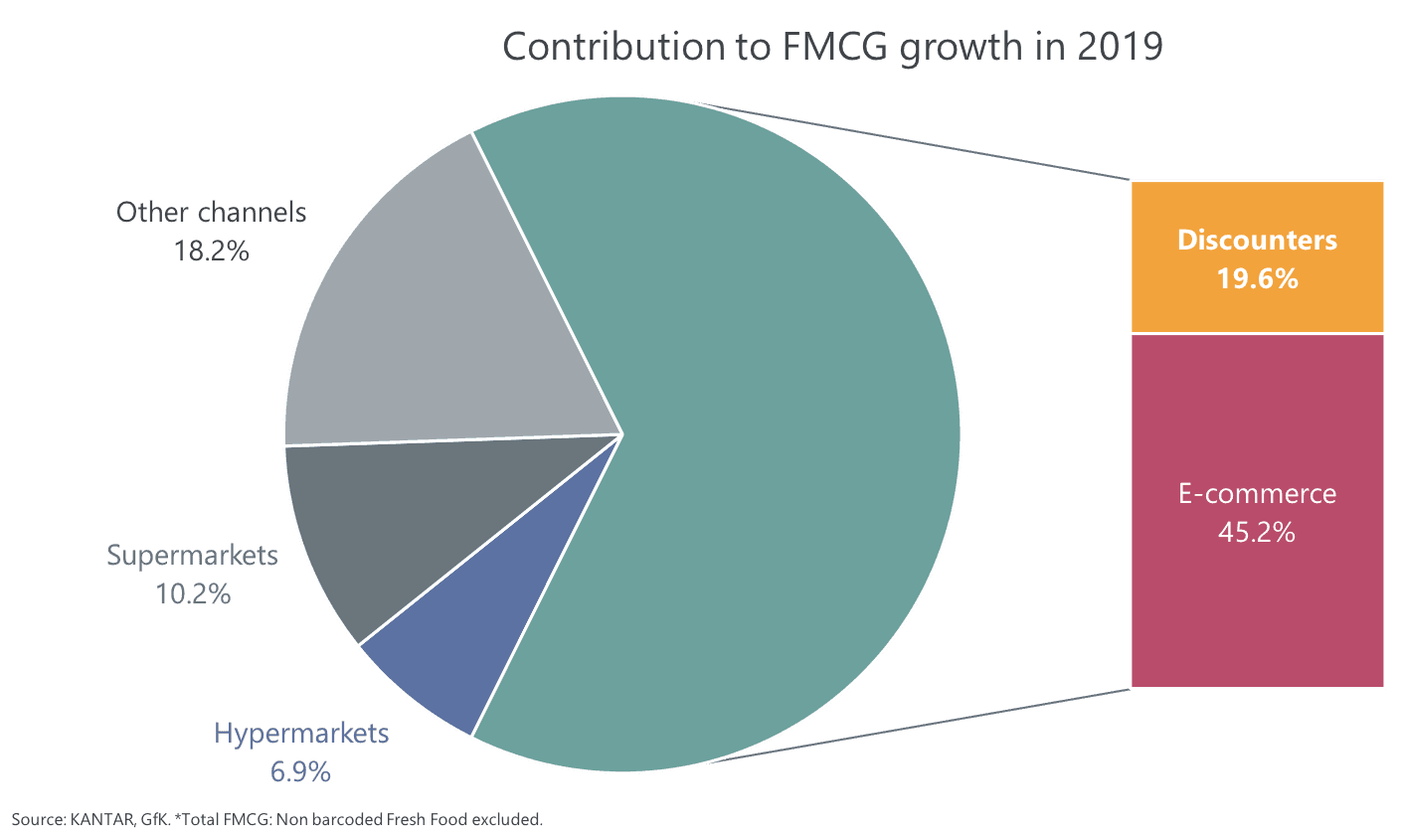

The data clearly indicates that next to E-Commerce Discounters are the only winners. While E-Commerce contributed 45.2% to the growth of the FMCG market in 2019, Discounters are the most successful brick and mortar channel with a contribution of 19.6%. Even combined, Hypermarket and Supermarkets add only 17.0% to the overall growth.

Who contributes to FMCG growth?

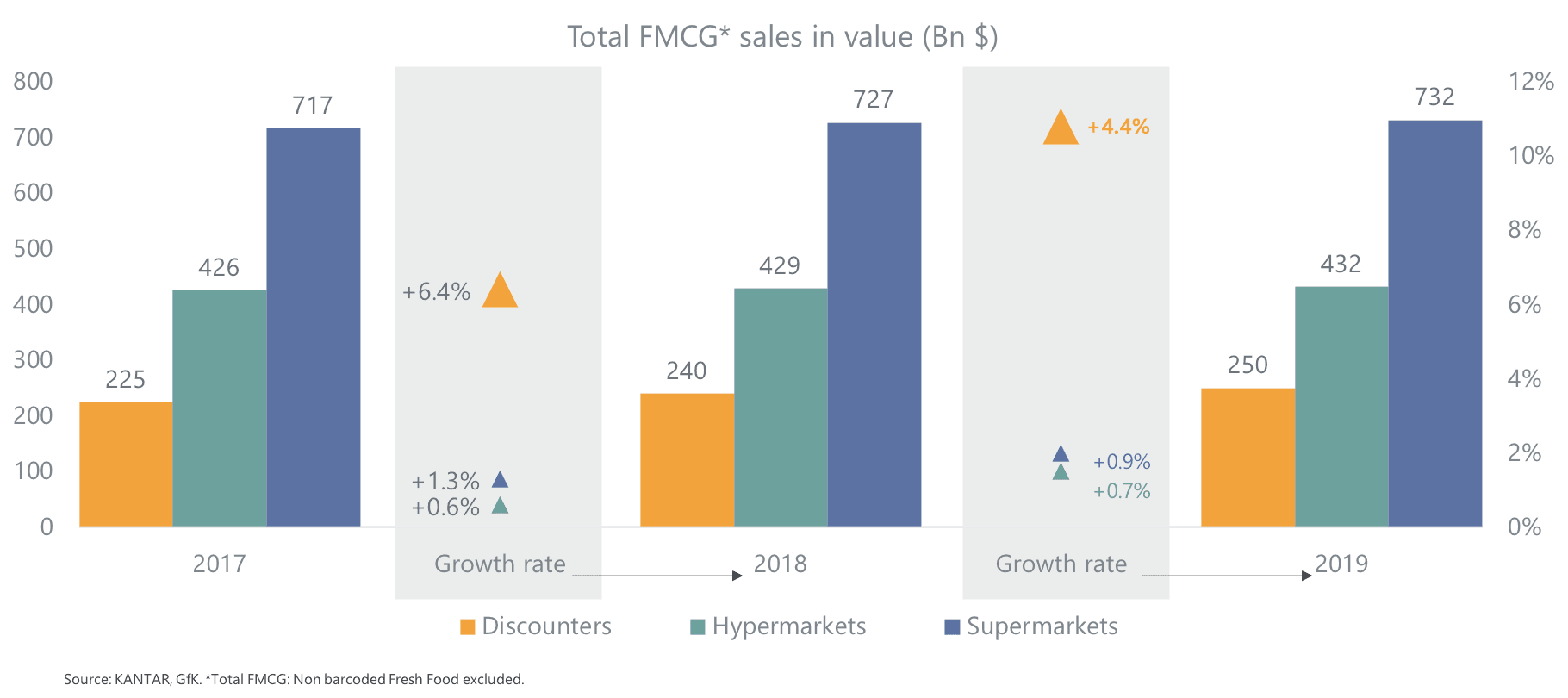

These numbers become even more significant if we compare global market share of Hypermarkets, Supermarkets and Discounters by taking a closer look at the value growth rate. While Discounters grew by +4.4% by value in 2019, Hypermarkets saw value growth of +0.9% and Supermarkets of +0.7%.

Additional data from the GfK and Kantar Consumer Panel support the picture, with Discounter winning on a global scale in 2019 (share of wallet +2,0%, number of trips per buyer +3,3%).

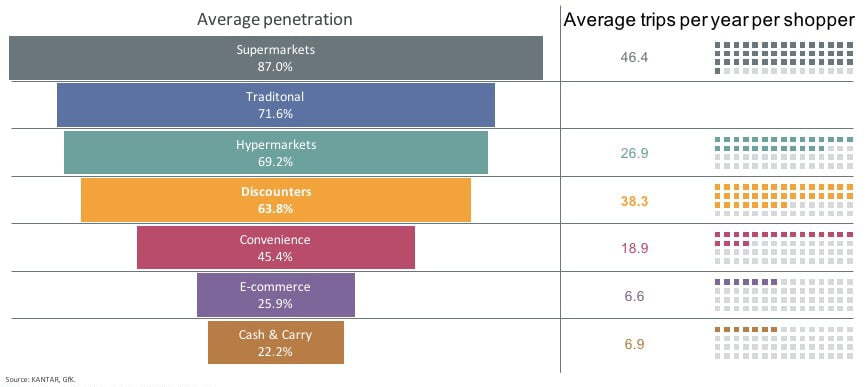

And there is room for growth: Our data for global average penetration see Supermarkets leading (87.0%), followed by Traditional (71.6%), Hypermarkets (69.2%), and Discounters (63.8%) ranked 4th. The number of trips per year per shopper sees Discounters placed No.2 (38.3) with 46.4 for Supermarkets. Therefore, increasing the number of trips could be another growth opportunity, with customer loyalty as one the key factors to succeed.

The message is simple: Around the globe, the decline of Hypermarkets and Supermarkets meets the rise of the Discounter. A closer look LATAM, the US, Asia and especially Western and Eastern Europe will add more color to this global development.

With Discounters – and E-Commerce – as the global winner in the global FMCG market, we take a closer look into the performance of the Discounters on the different continents.

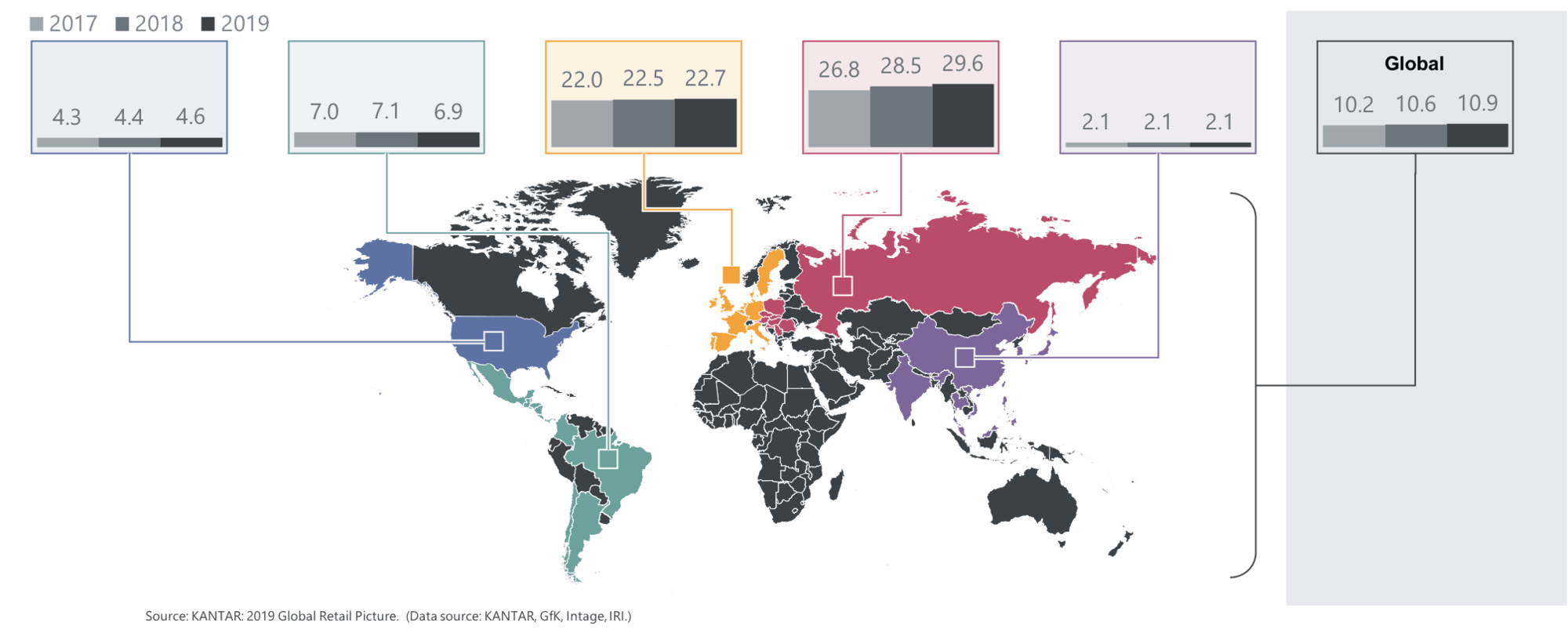

The numbers show a quite heterogeneous picture, with the value share for Discounters in 2019 ranging from 2.1% in Asia, 4.6% in the US, 6.9% in LATAM, to 22.7% in Western Europe and 29.6% in Eastern Europe.

A look into the development of the value share once again shows the steady growth of the Discounter on different continents: While we see single-digit growth in Asia (+1.5%) and Western Europe (+2.0%), Eastern Europe records a double-digit growth (+11.5%). LATAM faces a decline of -3.3%.

These growth rates for Discounters become even more significant if we look at the value share for the different channels. For example, the growth rate of +11.5% in Eastern Europe comes with a value share for Discounters of 29.6%, compared with 13.0% for Supermarkets and 16.9% for Hypermarkets. The growth rate of +2.0% in Western Europe has to be seen in relation to the strong position of Supermarkets (value share: 40.1%; value share Discounters: 22.7%; value share Hypermarkets: 17.5%). The data for Asia confirms the strength of the Supermarkets (value share: 26.9%) and Hypermarkets (value share: 12.9%) on this continent, compared to a value share of only 2.1% for Discounters.

The look at all continents allows us to summarize some key findings for the rise of the Discounters.

First of all, there is growth potential. With a clear strategy for market entrance or a precise growth strategy, Discounters should be able to significantly increase their value share in Asia, the US and LATAM. The strong value share in Eastern and Western Europe makes this continent the heartland of Discounters already.

Nevertheless, with a clear focus on their core strength – low price in combination with fulfillment of the latest needs of the consumer – Discounters should be able to continue on their growth path.

A deeper look into individual countries is perhaps the key to identifying patterns for Discounters on the rise.

Discounter market share in %