Picnic is a pure E-Commerce player, positioning itself as „Online Supermarket“. Founded in the Netherlands in 2015, the company expanded into Germany in 2018. While omnichannel retailer REWE is still the market leader in FMCG E-Commerce across Germany, Picnic has been extremely successful starting only in North Rhine-Westphalia and taking the lead in this region with currently more than 150.000 customers.

In an expert interview, Norman Buysse, Director Retail at GfK in the Netherlands, explains the key factors of Picnic’s success.

What is so special about Picnic? Why is it so successful? Looking at Picnic’s history helps to understand its strategy: When it was started, other retailers like online pioneer Albert Heijn, the #1 Supermarket in the Netherlands, already offered online grocery shopping, but the entry point for shoppers was rather high, with a high value basket for free delivery. Picnic made online more accessible for many shoppers, by lowering the minimum basket without delivery fees (minimum of 25 Euros) and by offering a more price aggressive assortment. Picnic teams with a retailer, in the Netherlands it started with Boni, in Germany with EDEKA, then decided to partner with EDEKA we will see that.

Picnic is a pure player. What differentiates Picnic from omnichannel retailers? It is difficult to compare, because Picnic’s strategy and the organization is very different from e. g. Albert Heijn or Jumbo, which offer their services country-wide. In simple words: what the App is for Picnic, is the brick-and-mortar store for all other Supermarket brands. Picnic is a technology company with an App and a shopping platform. The company is data-driven, like Google or Amazon, and knows its customers very well. In addition, focus of Picnic is on specific market regions, not striving for nationwide coverage. As a result, it can tailor the services, product range and the regions, it focuses on.

Who is the typical Picnic customer? For online groceries in general, initially it was the bigger, family household, fairly well-off, looking for convenience, a better work-life-balance. But with Picnic lowering the entry barrier, like no fee for smaller baskets, E-Commerce of FMCG also became attractive for smaller households, e. g. couples and the less wealthy. It was interesting to observe, that Albert Heijn has somewhat adapted to the entry points of Picnic.

Has COVID-19 changed FMCG shopping behavior in the Netherlands? Online was big and accelerating in the Netherlands even before COVID-19, and it has now seen a major push. To put online into perspective: This year, Supermarkets are expected to grow with an index of 110%, Specialist Groceries Stores with 125% and Online with 150%.

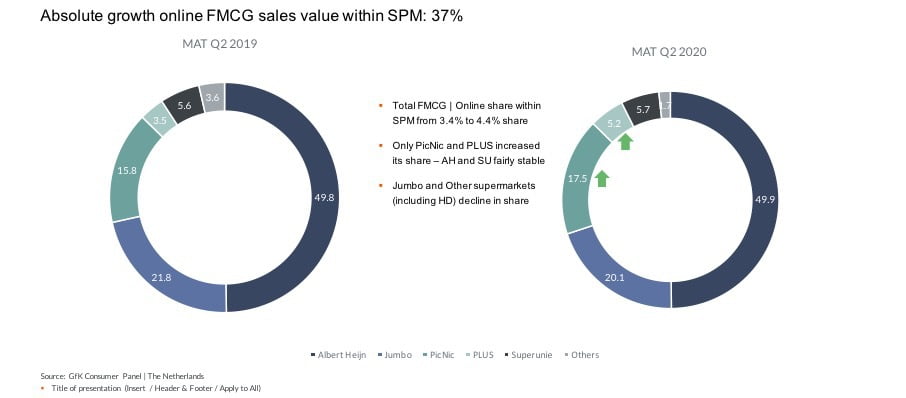

Do you see any challenges for Picnic in their expansion plans? It might sound strange, but Picnic’s biggest challenge is its success, its fast growth. Picnic now has a market share in E-Commerce for FMCG of 18% here. Compared to Albert Heijn 50% and Jumbo 20%.The biggest hurdle is scalability to ensure timely delivery, thus to meet the expectations of their clients: More home delivery means more days – more elapse time – for delivery. Frederic Knaudt, Co-founder of Picnic Germany recently said, that COVID-19 resulted in an extreme push for the company. At the beginning of 2020, the German organization had around 500 employees, by fall already 1500 and it was looking to hire another 400 to 500 people until yearend.

Absolute growth online FMCG sales value within SPM: 37%

COVID-19 started to hit Europe in February, with Italy being gravely affected as the first European country. As a consequence, Italy more or less froze public life on March 10, 2020, other European countries including Denmark and Germany followed with lockdowns within two weeks after.

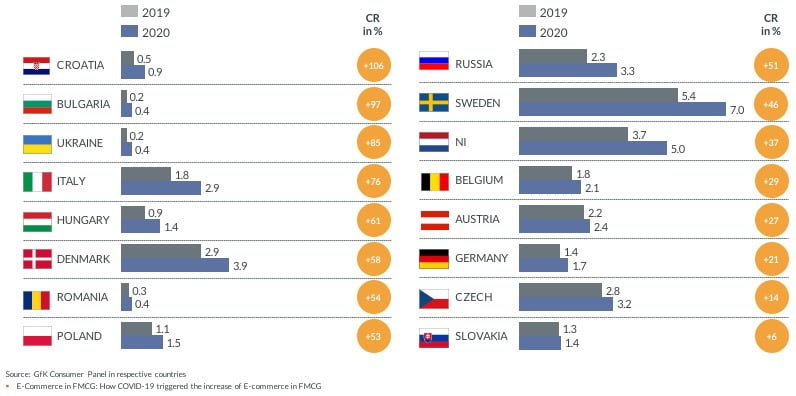

A comparison of the E-Commerce value shares of various countries for the period January to May 2019 and year-over-year 2020, clearly manifests the pandemic boost across Europe. Countries like Croatia and Bulgaria more or less doubled their E-Commerce value share (YoY), however on a fairly low level.

Looking at individual countries, the link between COVID-19 and the boost in E-Commerce becomes obvious. This is especially true for countries such as Italy and Denmark. Not surprisingly, Italy saw an increase in E-Commerce in FMCG of +76%, with a value share of 1.8% pre-COVID (Jan to May 2019) to 2.9% for the same period in 2020. Denmark, which already ranked among the leading E-Commerce countries in Europe with a value share of 2.9% in 2019, experienced a rise in online sales for FMCG by +58% to 3.9% for early 2020.

Countries like Austria, Belgium and Germany saw their countries being more or less locked down in March and April but were initially less affected by COVID-19 than e. g. Italy. These countries also observed a smaller increase in E-Commerce, still reaching between +21% (Germany), +27% (Austria) and +28% (Belgium). However, E-Commerce in FMCG continues to have a fairly small value share in all three countries. In May 2020 it reached 2.5% in Austria, 2.1% in Belgium and a mere 1.7% in Germany.

Sweden, which took a different route in fighting Corona, also displays an interesting development in the E-Commerce value share: Already in the lead in Europe with 5.4%, the country increased its E-Commerce in FMCG by +46% to a value share of 7.0%. Despite open shops during the first COVID-19 wave of 2020, it seems that more Swedish shoppers still preferred online over stationery shopping.

E-Commerce value share and change rate in %, Jan-May 2020 vs. 2019

Italy was hit early and very hard by COVID-19. In an interview, Marco Pellizzoni, Commercial Director, Consumer Panel & Services at GfK in Italy, provides additional insights into resulting changes in shopping behavior.

How do Italian shoppers feel about E-Commerce in FMCG? Outside FMCG, Italians are very open to Online as a shopping channel, resulting in very high market shares. Online grocery shopping has been growing, but the share was fairly small – before the pandemic. Fresh food plays a strong role in Italian habits, so the preference was on physical channels and even Traditional Trade. With COVID-19, this attitude changed considerably and growth in E-Commerce of FMCG accelerated: For example, penetration increased by more than 9 percentage points to 38.6% (March to October 2020 compared to same period 2019) and the average spend per trip rose from 135 to 180 Euros.

Who was the typical shopper before COVID-19 and now? In terms of demographics, no big changes compared to pre-COVID online shoppers: upper class, 35-54 of age, families with children. Currently E-Commerce in FMCG shows penetration peaks in North-West and Central Italy, due to the two big metropolitan areas Milan and Rome.

Is the exponential growth earlier this year only attributable to COVID-19? Looking at 2019, Italy was already on a strong growth path. But for sure, the recent acceleration was mostly due to the pandemic – however: In March only, when the first lockdown started, online could have reached a penetration of 30%, had there been enough capacity to deliver.

Who are E-Commerce retailers in Italy, more pure play or omnichannel? In Italy, we see more omnichannel retailers offering E-Commerce, with some pure players starting to gain traction, i. e. penetration. They offer a more selected range, rather than a general, wide assortment. Until last year, only Esselunga already had a strong online presence and positioning. Now several omnichannel retailers have a relevant incidence of online buyers in their total shopper base.

It seems that delays in delivery are particularly cumbersome for Italian shoppers – what are E-Commerce retailers in FMCG doing to address this? Retailers were just not ready for such a big acceleration in online demand. With the exception of retailers like Esselunga or Bennet, online was not a focus before the pandemic. Esselunga sent a letter of excuse for the delays to all clients, limited the number of online shopping instances, and reserved specific time slots for elderly and disabled clients. In addition, it offered “Click&Collect”. Another issue worth mentioning: In the first phase of the pandemic, websites of retailers saw an increase in visits of more than +200%, as people were looking for online options. But most of the websites were not at all up-to-date, just featuring generic information, more or less nothing on products or prices. This has changed. Now, retailers are putting more emphasis on online, offering home delivery, Click&Collect or Drive Thru options. Some pure players, for example, are giving priority to grocery purchases over non-food during the lockdown period.

Covid period: March-October

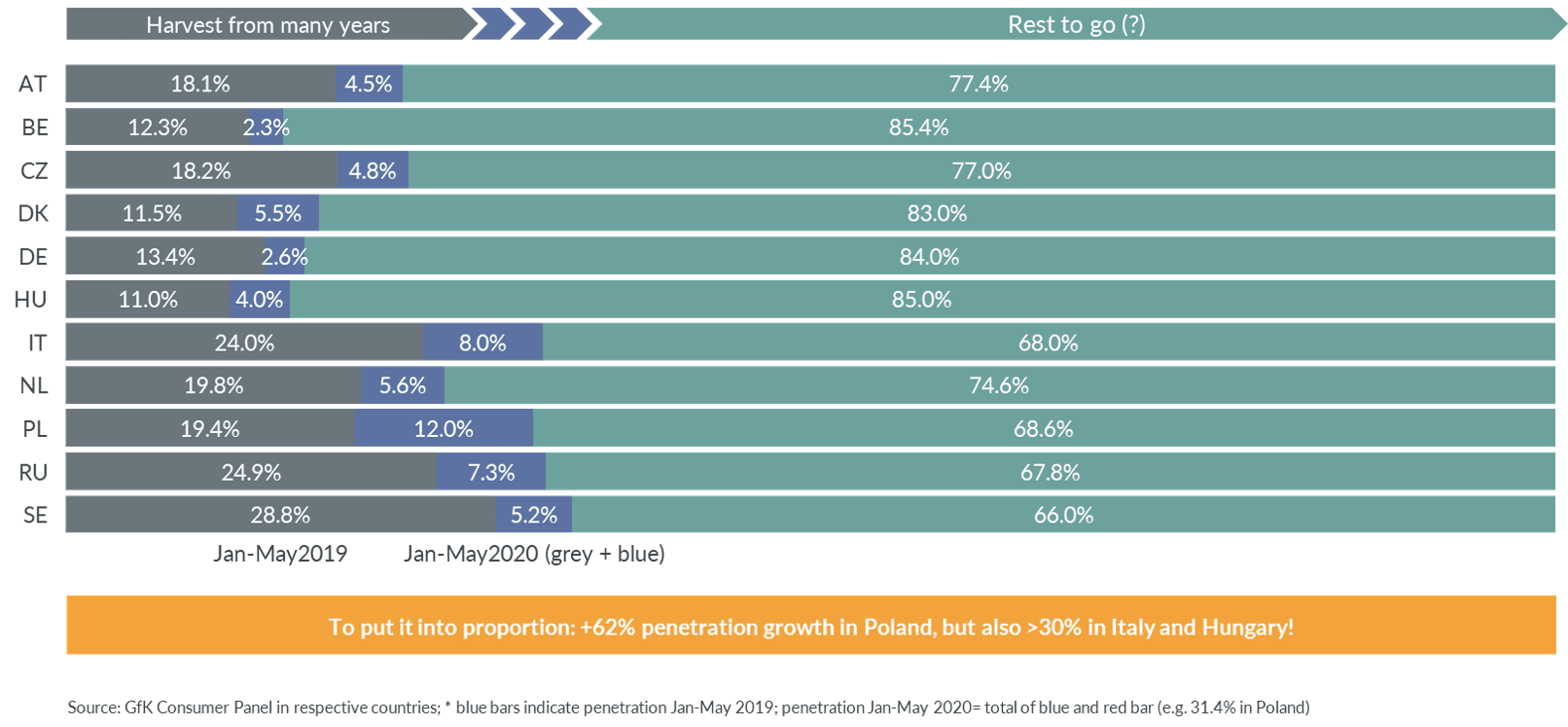

FMCG E-Commerce penetration in %, Jan-May 2019 and Jan-May 2020*

Of course, value growth goes hand in hand with channel penetration. It seems logical, that the first five months of 2020 also resulted in a considerable increase in E-Commerce penetration and new groups of buyers being attracted to shop FMCG online. Whereas before – as surveys in 2019 documented – high convenience was the decisive argument for choosing the online channel, it has now shifted to precaution, a measure of health and safety.

Again, Italy and Denmark rank among the growth giants: E-Commerce penetration in Italy rose by one third between January and May 2020, reaching 32% (In 2019: 24%).

Denmark put on nearly +50% compared to 2019, now achieving a channel penetration of 16% (2019: 11.5%). But both countries are dwarfed by Poland, which increased E-Commerce penetration by +62% year over year, moving from 19.4% (Jan to May 2019) to 31.4% in 2020.

Only two countries are still doing better: Russia, reaching an E-Commerce penetration for FMCG of 32.2% and again Sweden ahead at 34%, whereas Germany, for example, only reaches 16% to date and Belgium 14.6%, both showing an increase of +19% (YoY).

With the COVID-19 pandemic currently aggravating health hazards across Europe, it is easy to predict a further acceleration in market penetration and it will be interesting to see, whether the discrepancies between European countries will persist.

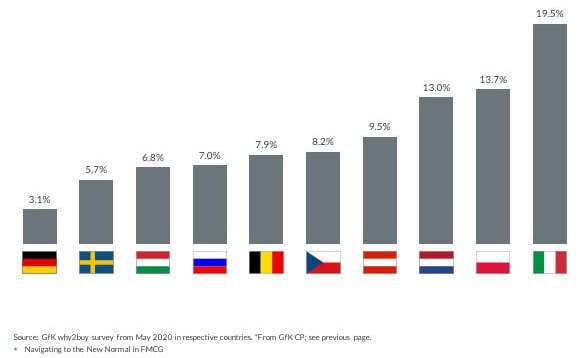

The COVID-19 pandemic pushed E-Commerce in FMCG, but there could have been more growth. The main obstacle that discourages shoppers to source their daily groceries online has been the delay in delivery.

Many European said that they would have ordered groceries online if the delivery time had been shorter. In Italy, for example, this could have meant nearly +20% more customers and a potential E-Commerce penetration above 50%.

The good news is, that shoppers remain open to the idea of buying FMCG online and are willing to try again when offered better delivery conditions after the COVID-19 pandemic.

In order to avoid the delivery challenge, more and more omnichannel players offer a so-called “Click&Collect” service, where shoppers order their products online and pick them up in stationary outlets. Whereas this form of “hybrid” shopping is not new to some countries such as the UK and France, numerous German retailers jumped on the bandwagon in the past months.

This could help them improve the “online balance sheet”: Lionel Souque, CEO of Rewe Group, recently conceded* that E-Commerce in FMCG was still a loss-making business, and Rewe aims to reach up to 90% of households via Click&Collect, up from an actual 40%. Hence, Click&Collect could be the solution for a lasting increase in E-Commerce penetration and shoppers’ loyalty to this channel.

Timely delivery is the main stumbling block for E-Commerce in FMCG. Click&Collect holds the promise to overcome this barrier, at the same time offering omnichannel retailers to closely integrate stationary and online. Benefits for grocery shoppers include

Whereas this cross-channel approach certainly appeals to omnichannel retailers, who obviously avoid any delivery challenges, the question remains, if shoppers in the long run really regard this concept as convenient.